Hiring a single remote employee in Asia can accidentally create a taxable presence, a permanent establishment, for your entire company. The OECD's November 2025 update to the Model Tax Convention changed how this is assessed. Here is the country-by-country playbook for the 12 APAC markets where it matters most, written as an operational compliance reference for tax directors, finance leads, and founders working alongside their tax advisors.

|

6 Key Takeaways

|

| Permanent establishment (PE) risk is the chance that a single remote employee creates a taxable corporate presence for your company in their country. |

| PE thresholds vary widely across Asia. A 30-day visit triggers different exposure in Japan than in Singapore and India. |

| The OECD's November 2025 Model Tax Convention update introduces a new two-part framework, a 50% working-time temporal test, and a commercial reason test for assessing PE in cross-border remote work cases. |

| Three PE types matter: fixed place PE, dependent agent PE, and (in some treaties) service PE. Each has different triggers. |

| A common operational approach is to employ remote APAC workers through a local entity or an Employer of Record, which shifts the legal employer relationship to a local entity and changes how PE attribution is analyzed. |

| Slasify operates an APAC-strong EOR with in-country partners across Singapore, Japan, South Korea, China, Hong Kong SAR, Taiwan, Vietnam, Indonesia, Malaysia, Thailand, the Philippines, and India. |

1. What is permanent establishment (PE) risk?

A permanent establishment (PE) is a tax concept that determines whether a foreign company has enough business presence in a country for that country to tax its profits. If your company crosses the PE threshold, the host country gains the right to tax the portion of your profits attributable to local activities, even if you never registered an entity there.

Three PE types matter for remote work in Asia:

- Fixed-place PE. A physical location, office, branch, factory, or, in some cases, an employee's home office, that is at the disposal of the foreign company and used for its business continuously.

- Dependent agent PE (DAPE). An individual in the host country who habitually concludes contracts on the company's behalf, or who habitually plays the principal role leading to contract conclusion.

- Service PE. A treaty-specific concept that creates a PE when the company furnishes services in the host country through employees or other personnel for more than a defined day count, typically 90 to 183 days within 12 months.

The consequences of triggering PE are not theoretical. They include corporate income tax registration, transfer pricing documentation, profit attribution, payroll withholding, and, in many cases, social security obligations, retroactive to the day the PE arose. Penalties and interest are common where the PE was discovered through an audit rather than disclosed voluntarily.

2. Why remote workers in Asia trigger PE risk

Three operational patterns drive most APAC PE cases we see:

-

The home office trap (fixed place PE). An employee works for your foreign entity from their apartment in Tokyo, Seoul, or Bangalore. If that home is used continuously to carry on the business of the enterprise, tax authorities can argue it is a fixed place at the company's disposal. The longer and more structurally embedded the arrangement, the higher the risk.

-

The sales rep problem (dependent agent PE). A remote employee in Singapore, Jakarta, or Mumbai meets with local prospects, negotiates terms, and effectively closes deals, even if the contract is formally countersigned at headquarters. Most APAC tax authorities follow the OECD-aligned "principal role leading to conclusion" test, which captures sales activity in substance, not just in form.

-

The service hours problem (service PE). Engineers, consultants, or implementation specialists who deliver services in a host country accumulate days against a treaty-specific threshold. Cross the line, and the company has a service PE even with no office, no agent authority, and no fixed location.

A remote employee can sit at the intersection of all three. That is why a "we just pay them as a contractor from abroad" structure rarely survives scrutiny once the relationship is long-term, full-time, or revenue-facing.

-1.jpg?width=1080&height=1080&name=Untitled%20design%20(6)-1.jpg)

Based in Singapore, Slasify has built out an ISO 27001-certified, KPMG-recognized payroll and Employer of Record (EOR) network across the region since 2016, with over 600 local partners across Asia. We work alongside in-house tax teams and external advisors, including the Big 4 firms, on hundreds of these conversations a year.

3. What the OECD November 2025 update changed

-3.jpg?width=1920&height=1080&name=Blog%20Post%20Banner%20%26%20Images%20(1)-3.jpg)

On 19 November 2025, the OECD published the 2025 Update to the Model Tax Convention, the first comprehensive revision since 2017. The most significant changes update the Commentary on Article 5, the Permanent Establishment provision, to address cross-border remote work.

The update introduces a two-part analytical framework for whether a home or other personal location can be a fixed place of business PE.

The temporal test

If a remote employee works from a home or similar non-company location for less than 50% of their total working time over any 12 months, the location is generally not considered a fixed place of business. No fixed place, PE arises on that basis alone. This is a safe harbor for incidental remote work, short relocations, and digital nomad arrangements.

The commercial reason test

If the employee crosses the 50% threshold, the analysis moves to whether there is a genuine commercial reason for the business to be carried on from that country. Commercial reasons include serving local clients, developing a local market, supporting real-time service delivery in a relevant time zone, or accessing local expertise. Personal convenience, employee preference, and family relocation do not, on their own, constitute commercial reasons.

What did not change

The 2025 update does not alter the dependent agent PE analysis. Habitually concluding contracts (or playing the principal role in their conclusion) on behalf of a foreign company remains a PE trigger regardless of working-time percentages. It also does not override individual country laws or specific bilateral tax treaties.

Pre- and post-update framework at a glance

|

Element

|

Pre-November 2025

|

Post-November 2025

|

|

Fixed the place PE from the home office

|

Fact-driven, limited Commentary guidance (2 paragraphs since 2012)

|

Structured two-part test with 5 pages of new Commentary and examples

|

|

Time threshold

|

No quantitative benchmark

|

50% of working time over 12 months

|

|

Qualitative test

|

Disposal test only

|

Disposal + commercial reason test

|

|

Dependent agent PE

|

Unchanged

|

Unchanged

|

|

Service PE in specific treaties

|

Unchanged

|

Unchanged

|

A practical caveat: the OECD Commentary is interpretive, not binding. Several countries, including India and Malaysia, have indicated they will not adopt the new tests in full. Local law and the specific bilateral treaty always govern. As of May 2026, most APAC tax authorities have not yet issued formal guidance aligning with the 2025 update.

4. PE risk by country: the APAC playbook

The table below summarizes the headline PE thresholds for the twelve APAC markets where we most often see remote-work questions. Each row is sourced to the country's primary tax authority and the relevant bilateral treaty. Treat this as a triage map, not a substitute for jurisdiction-specific advice.

APAC PE risk thresholds at a glance

The table below summarizes the headline PE thresholds for the twelve APAC markets, strictly reflecting the latest 2026 version of local regulations and tax treaties.

|

Country

|

Fixed place PE trigger

|

Dependent agent PE

|

Service PE threshold

|

US tax treaty?

|

Primary regulator

|

|

Singapore

|

Fixed place of business; OECD-aligned definition in DTAs

|

Habitual conclusion of contracts

|

Treaty-specific; building/installation >183 days under typical DTAs

|

No (no US-Singapore DTA)

|

IRAS

|

|

Japan

|

Fixed place; home office may qualify if continuous

|

Dependent agent with contracting authority

|

Construction >1 year (domestic); treaty-specific service PE in some DTAs

|

Yes

|

NTA

|

|

South Korea

|

Fixed place; includes location where services rendered >6 months in 12 consecutive months

|

Habitual contract conclusion or principal role

|

6 months in 12 consecutive months (domestic)

|

Yes

|

NTS

|

|

China (mainland)

|

Fixed place of business

|

Dependent agent

|

6 months under US-China DTA (older treaty); 183 days under newer DTAs (e.g., Singapore, Hong Kong)

|

Yes (6-month rule)

|

STA

|

|

Hong Kong SAR

|

Permanent place of business in HK

|

Habitual contract conclusion

|

Treaty-specific; territorial source system limits scope

|

No (no US-HK DTA)

|

IRD

|

|

Taiwan

|

Fixed place of business in Taiwan

|

Dependent agent

|

Generally, 183 days under the DTAs that Taiwan has signed

|

No comprehensive US-Taiwan DTA (special arrangements under discussion)

|

NTBT

|

|

Vietnam

|

Fixed place of business

|

Authority to sign contracts or regularly deliver goods/services

|

183 days in any 12-month period (domestic and most treaties)

|

No

|

GDT

|

|

Indonesia

|

Fixed place of business

|

Dependent agent

|

60 days in 12 months (domestic); 183 days under most treaties

|

No

|

DJP

|

|

Malaysia

|

Fixed place of business

|

Habitual contract conclusion or principal role

|

Treaty-based, typically 183 days in 12 months

|

Yes (limited)

|

LHDN

|

|

Thailand

|

Fixed place; "carrying on business" test under domestic law

|

Agent with contracting authority

|

90 days in 12 months under the US-Thailand DTA (30-day de minimis)

|

Yes

|

RD

|

|

Philippines

|

Fixed place of business

|

Dependent agent

|

Generally, 183 days under most DTAs

|

Yes

|

BIR

|

|

India

|

Fixed place; aggressive interpretation of "virtual" presence

|

Habitual contract conclusion; "principal role" added under MLI

|

90 days in 12 months under US-India DTA (30 days if related party); 6 months under some other DTAs

|

Yes

|

ITD

|

As of May 2026. Treaty thresholds reflect the most commonly invoked bilateral agreements with the United States. Thresholds may differ under treaties with other home jurisdictions. Find your Employment Guide for Asia and plan your global payment strategically.

4.1 Singapore

The Inland Revenue Authority of Singapore (IRAS) defines PE broadly under domestic law, but most cross-border cases turn on the relevant Double Tax Agreement (DTA) rather than the wider domestic definition. Singapore does NOT have a comprehensive tax treaty with the United States, so US-headquartered companies cannot rely on treaty thresholds and must look at Singapore's domestic rules and the OECD-aligned definitions in IRAS guidance. Practically, a long-term remote employee performing core revenue functions from a Singapore home office, particularly with contract authority, creates a credible fixed place or agency PE argument. The 60-day rule for individual taxation is unrelated to corporate PE risk and should not be confused with it.

Learn about the global hiring and payment landscape with our Singapore Employment Guide.

4.2 Japan

Japan's PE framework, administered by the National Tax Agency (NTA), aligns closely with Article 5 of the OECD Model. There is no specific day-count threshold for fixed place PE under domestic law, but the OECD Commentary's 6-month indicator is widely used. A home office used continuously for the employer's business can constitute a branch PE, particularly where the employee's role is core rather than auxiliary. Construction or installation activities exceeding one year trigger a domestic-law PE. In our experience, the highest-risk Japan profiles are senior commercial roles, country managers, and engineering leads working from Tokyo or Osaka homes on a long-term basis.

Read our Japan Employment Guide for in-depth context on how to hire and pay remote employees in Japan.

4.3 South Korea

The National Tax Service (NTS) applies a clearly defined service rule. A fixed place PE includes any location where employees of a foreign corporation provide services for more than six months within any 12 consecutive months, or where similar services are rendered continuously or repeatedly for two or more years, even if each engagement is shorter. The dependent agent rule was tightened under Korea's BEPS-aligned amendments and captures habitual "principal role" activity. South Korea is one of the most active APAC jurisdictions for PE audits of foreign companies with Korean remote staff.

Discover the global hiring and employment landscape in South Korea.

4.4 China (mainland)

-Jun-24-2026-07-40-58-0476-AM.jpg?width=1920&height=1080&name=Blog%20Post%20Banner%20%26%20Images%20(1)-Jun-24-2026-07-40-58-0476-AM.jpg)

The State Taxation Administration (STA) administers PE rules through both domestic law and 100+ bilateral DTAs. The service PE threshold varies materially by treaty: older treaties (including the US-China DTA) apply a six-month rule, while newer treaties (Singapore, Hong Kong SAR, Macau, Belgium, Finland) apply a 183-day rule. The six-month rule is the more aggressive of the two; presence for a single day in a calendar month is treated as a full month for counting purposes under the older formulation. Multiple employees working in China on the same day count as a single day. China is documentation-driven, and PE audits commonly examine the substance of secondment arrangements.

Learn about the global hiring and payment landscape with our China Employment Guide.

4.5 Hong Kong Special Administrative Region (Hong Kong SAR)

The Inland Revenue Department (IRD) operates under a territorial tax system. Corporate income is taxed only if it has a Hong Kong source, which substantially reduces PE-driven exposure compared with worldwide tax jurisdictions. PE remains relevant for treaty purposes, but Hong Kong SAR does not have a comprehensive tax treaty with the United States. Direct hiring of a remote employee in Hong Kong typically requires either local entity registration or an EOR arrangement to handle Mandatory Provident Fund (MPF) contributions and salaries tax withholding.

Learn about the global hiring and payment landscape with our Hong Kong Employment Guide.

4.6 Taiwan

The National Taxation Bureau of Taipei (NTBT) applies a PE framework aligned with the OECD model under Taiwan's bilateral DTAs. There is no comprehensive US-Taiwan income tax treaty as of May 2026, although discussions on a US-Taiwan tax agreement have been ongoing. In the absence of treaty coverage, Taiwan domestic law governs, and substantive commercial activity by a Taiwan-based remote employee creates real fixed place and agency PE exposure. The 183-day individual residency threshold is separate from corporate PE analysis.

Learn about the global hiring and payment landscape with our Taiwan Employment Guide.

4.7 Vietnam

Vietnam's General Department of Taxation (GDT) operates under a particularly broad domestic PE definition. Under the Corporate Income Tax Law, a PE includes any service-providing establishment, including consultancy, where services in connection with a project or projects in Vietnam exceed 183 days in any 12-month period. Representatives in Vietnam with authority to sign contracts, or who regularly deliver goods or services, also create PE. The Vietnamese definition is wider than the OECD model and is interpreted with limited deference to commercial substance arguments.

Learn about the global hiring and payment landscape with our Vietnam Employment Guide.

4.8 Indonesia

-Jun-24-2026-07-43-09-7558-AM.jpg?width=1920&height=1080&name=Blog%20Post%20Banner%20%26%20Images%20(2)-Jun-24-2026-07-43-09-7558-AM.jpg)

The Directorate General of Taxes (DJP) applies the lowest service PE threshold in our APAC table. Indonesian domestic law treats services provided in Indonesia for more than 60 days within a 12-month period as a PE trigger, although bilateral treaties typically raise this to 183 days. The domestic threshold matters when no treaty applies, or where the treaty does not contain a service PE clause. Indonesia also requires PE-level registration, withholding tax, and, in many cases, VAT registration once the PE is constituted.

Learn about the global hiring and payment landscape with our Indonesia Employment Guide.

4.9 Malaysia

The Inland Revenue Board (LHDN) determines PE primarily through tax treaties, with domestic law providing a broader fallback "place of business" definition. Most Malaysian treaties contain a service PE clause with a 183-day threshold in any 12-month period. The dependent agent definition under Malaysian treaties has been updated through the Multilateral Instrument (MLI) to include the "principal role" test, capturing sales activity that effectively closes deals even where a formal signature happens abroad. Malaysia has indicated it will not adopt the OECD 2025 home office tests in full, so the home office position in Malaysia is best assessed on local-law grounds.

Learn about the global hiring and payment landscape with our Malaysia Employment Guide.

4.10 Thailand

The Revenue Department (RD) applies a "carrying on business" test under domestic law and PE-based taxation under treaties. The US-Thailand DTA contains one of the lower service PE thresholds in the region: 90 days in any 12-month period, with a de minimis exclusion where services are rendered for fewer than 30 days in a taxable year. Construction and installation projects trigger PE after 120 days. Thailand is also notable for its work permit regime, which interacts with PE analysis where remote workers lack an appropriate immigration status.

Learn more about the global hiring and payment landscape with our Thailand Employment Guide.

4.11 Philippines

The Bureau of Internal Revenue (BIR) administers PE rules through over 40 bilateral DTAs, most of which align with the OECD model. The standard service PE threshold under the Philippines treaties is 183 days in 12 months. Where no treaty applies, domestic "doing business in the Philippines" rules can produce broader exposure. The Philippines is one of the larger remote-work destinations in the region, and remote employees in long-term, full-time roles for foreign employers are a recurring PE question.

Learn about the global hiring and payment landscape with our Philippines Employment Guide.

4.12 India

-Jun-24-2026-07-47-00-2509-AM.jpg?width=1920&height=1080&name=Blog%20Post%20Banner%20%26%20Images%20(3)-Jun-24-2026-07-47-00-2509-AM.jpg)

India operates the most aggressive PE regime in our APAC table. The Income Tax Department (ITD) and Indian courts have consistently applied a wide interpretation of fixed place, agency, and service PE. The US-India DTA contains a 90-day service PE threshold in any 12 months, reduced to 30 days where services are performed for a related enterprise. Indian tax authorities have also tested "virtual service PE" arguments in court. While the Delhi High Court in late 2025 confirmed that physical presence is required to count days under the India-Singapore treaty, the audit posture remains aggressive. India has formally indicated it will not accept the OECD 2025 home office tests, so the OECD safe harbor offers little practical protection in India.

Mapped your APAC PE exposure with your tax advisor, and need to put the operational structure in place? Chat with our team to see how an Employer of Record can shift the legal employer relationship to a local entity and significantly mitigate the PE risk attributable to your remote APAC hires.

5. The three operational paths to manage PE risk

Once your tax advisor has identified the PE exposure profile for a given role and country, there are three credible structures for paying remote APAC employees compliantly, plus one widely used arrangement that requires a strong health warning. The right choice is a function of headcount, time horizon, and your advisor's reading of the specific treaty and country position.

|

Approach

|

PE risk profile

|

Setup time

|

Cost profile

|

Best for

|

|

Direct hire from a foreign entity

|

Higher exposure. Depending on the role, it can give rise to fixed place, agency, or service PE arguments

|

Days (operationally), but exposure analysis begins immediately

|

Low upfront, potentially significant if PE is assessed retroactively

|

Short-term arrangements only, where confidence in non-PE status is documented and supported by counsel

|

|

Set up a local entity

|

Substantially changes the analysis (the local entity becomes the employer), but creates a full local corporate tax footprint of its own

|

3 to 6 months in most APAC markets

|

Initial setup: USD 5,000 to 30,000+; ongoing: USD 20,000 to 100,000+ per year per country

|

Companies committing long-term to a market with multiple hires planned

|

|

Employer of Record (EOR)

|

The EOR is the legal employer locally; the worker's activities are attributed to the EOR rather than to the client, which significantly mitigates the client's PE exposure

|

1 to 4 weeks is typical

|

Per-employee monthly fee; no entity costs

|

Hiring 1 to 20 employees per country, or testing a market

|

|

Contractor (independent)

|

Misclassification risk and dependent-agent PE risk if the contractor acts substantively as an employee or sales agent

|

Immediate

|

Low

|

Genuinely independent specialists for defined, time-bound scopes

|

The contractor route is the one we see most often misused. A long-term, full-time, exclusive remote "contractor" in Vietnam, India, or the Philippines, paid monthly with a fixed scope and integrated into the client's reporting line, is almost always able to be reclassified as an employee under local law. The PE exposure is then layered on top of the misclassification exposure. Our convert contractor to employee guide covers the operational fix.

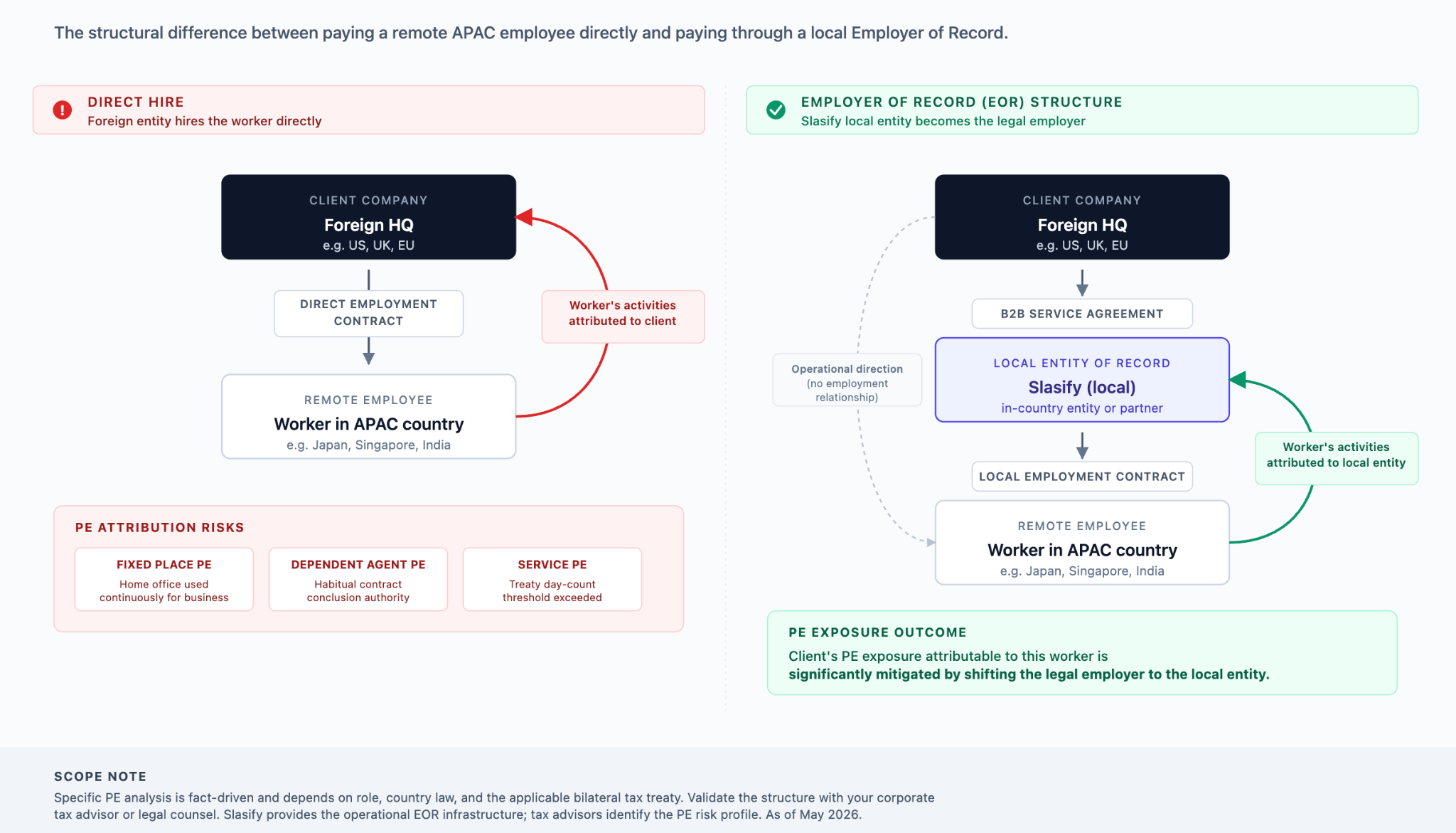

6. How an Employer of Record shifts the legal employer relationship

The mechanics of an EOR are straightforward, and the reason it changes the PE analysis is structural, not contractual. An EOR does not eliminate corporate tax liability in any absolute sense; what it does is shift who is the legal employer in the host country, which in turn shifts where the worker's activities are attributed for PE purposes.

When a company hires through Slasify's EOR:

- The client signs a B2B service agreement with Slasify. Slasify is the service provider, and the client is the customer. No employment relationship exists between the client and the worker.

- Slasify (or our in-country partner of record) signs a local employment contract with the worker, in the local language, under local employment law, with statutory benefits, social security, and tax withholding.

- The client retains day-to-day operational direction over the worker's tasks, deliverables, and performance, while Slasify carries the legal employment relationship.

- Slasify invoices the client monthly for salary, benefits, employer contributions, and our service fee.

Because the worker is employed by a local entity in the host country, and that entity (Slasify or our partner) is the one with personnel, payroll, and contracting authority on the ground in its own name, the worker's employment activities are attributed to the EOR. The client has no employment relationship with the worker, no fixed place in its own name, and no personnel of its own in the host country. This significantly mitigates the client's PE exposure attributable to the worker, although the specific PE analysis remains fact-driven, and your tax advisor should still validate the structure for your particular facts, role profile, and treaty position.

This is materially different from the contractor route, where the client itself is the counterparty to the worker. It is also materially different from "shadow payroll" or non-resident employer arrangements, which manage tax withholding but do not change the underlying employer-of-record analysis.

Where the EOR sits in your compliance stack, we work most effectively alongside in-house tax teams and external advisors, including the Big 4. The typical workflow looks like this:

- Your tax advisor or legal counsel assesses the PE risk profile of a planned hire under the applicable treaty and country law.

- You decide whether direct hire, local entity setup, contractor management, or EOR is the right structural answer for the role.

- Slasify executes the EOR path where that is the chosen approach, providing the local employment contract, statutory benefits, payroll, social security, and tax withholding through our entity or in-country partner of record.

This division of labor matters. Tax advisors identify what the risk is; an EOR provides the operational infrastructure to give effect to a particular risk-mitigation structure.

"We had a US-based SaaS partner in late 2025 who placed a senior engineering lead in Tokyo. They had been planning a direct hire from the US entity, paid out of the US payroll. Their external tax advisor flagged the Japan branch PE risk under Japan domestic law, where a continuously-used home office for core business activities can constitute a fixed place PE. We didn't change their tax position; the advisor did the analysis. What we did was give them a Japan EOR structure that materially shifted the employment relationship to our local entity, in line with the advisor's recommendation, within a week. The hire still started on schedule." – Slasify Account Manager

7. Compliance checklist before paying any remote APAC employee

Before payroll runs for the first time, walk through this checklist with your tax and legal advisors:

- Identify the host country and the home country. Confirm whether a bilateral tax treaty exists, and pull the PE article (typically Article 5) and the dependent personal services article (typically Article 15).

- Map the role's substance. Is the employee revenue-facing, contract-touching, service-delivering, or back-office? The same employee on paper can trigger or avoid PE depending on actual day-to-day activity.

- Estimate days in the country over a rolling 12-month period. Service PE thresholds run on a 12-month, not calendar-year, basis in most APAC treaties.

- Assess the home office. Continuous use over 12 months for the employer's business is the OECD 2025 fixed-place test. Document whether the company directs the work location.

- Review the contracting authority. Does the employee negotiate, sign, or play the principal role in concluding contracts? If yes, the dependent agent PE is in scope, independent of working-time tests.

- Check the country's adoption of the OECD 2025 update. Several APAC tax authorities, including India and Malaysia, have indicated they will not apply the new tests as written.

- Confirm payroll, social security, and individual tax obligations. PE analysis is corporate-level; individual tax residency and employer withholding can apply even where no PE arises.

- Choose the structure. Direct hire, local entity, EOR, or contractor. Document the rationale.

For a broader cross-border compliance context, our payroll tax compliance guide and termination laws by country guide cover the downstream operational layers.

Hire anywhere in Asia. Execute the compliant structure.

Once your tax advisor has mapped your APAC PE exposure, the operational fix is usually a one-week conversation, not a one-year reorganization. Slasify's EOR and Global Payroll services provide the local employment infrastructure to execute the structure your advisor has recommended, across the twelve APAC countries above, with one platform, 130+ currencies, and 600+ local partners.

Stop guessing about your permanent establishment exposure. Book a free consultation with our APAC compliance experts today to design a fully compliant, risk-mitigated EOR structure for your remote workforce.

8. FAQs About Permanent Establishment Risks in Asia

Q1. What is permanent establishment risk?

Permanent establishment risk is the chance that your company's activities in a foreign country, including those of a single remote employee, cross the threshold at which that country can tax your business profits. Once a PE exists, the foreign tax authority can assess corporate income tax on profits attributable to the PE, plus require registration, transfer pricing documentation, and ongoing compliance filings.

Q2. Can a single remote employee trigger PE for my company?

Yes, in principle. A single employee can give rise to a fixed place PE argument (through continuous home-office use), a dependent agent PE argument (through habitual contract conclusion), or a service PE argument (through accumulating service days under a treaty), independent of whether your company has any other presence in the country. Whether any of these arguments succeed depends heavily on the specific country, the role, the duration, and the bilateral treaty. Your tax advisor should map the exposure for your particular situation.

Q3. How many days can an employee work in Japan before creating PE?

There is no fixed day count under Japanese domestic law for fixed place PE. The OECD Commentary's 6-month indicator is widely used as a guideline, and construction or installation activities exceeding one year trigger PE under domestic rules. For service PE, you need to check the specific bilateral treaty. The safer benchmark is to assume that continuous full-time remote work from a Japanese home office over six or more months creates meaningful PE risk.

Q4. Does hiring a remote contractor in Asia create PE risk?

Yes, in several scenarios. If the contractor habitually concludes contracts on your behalf or plays the principal role leading to contract conclusion, a dependent agent PE can arise. If the contractor is, in substance, an employee under local law, misclassification rules can recharacterise the relationship, and PE exposure can layer on top. Genuinely independent contractors with multiple clients and defined scopes carry lower (but non-zero) risk.

Q5. How does an Employer of Record help mitigate permanent establishment risk?

An Employer of Record (EOR) structurally shifts the legal employment relationship, significantly mitigating PE risk for the parent company. Here is how it breaks down:

- B2B Agreement: You sign a service agreement with the EOR, meaning you have no direct employment footprint in the host country.

- Local Employment: The EOR acts as the legal employer, managing local payroll, personnel, and compliance.

- Risk Transfer: Because the employment relationship sits locally with the EOR, the worker's activities are attributed to the EOR rather than your foreign headquarters.

Q6. What did the OECD's November 2025 update change about PE?

The OECD's November 2025 update added a two-part framework to the Commentary on Article 5 for assessing when a home office or similar location can be a fixed place of business. The first test is temporal: less than 50% of working time over a 12-month period generally does not create PE. The second test, applied if the 50% threshold is crossed, is whether there is a commercial reason for the business to be carried on from that country. The update did not change the dependent agent PE rules or specific treaty service PE thresholds.

Q7. Which APAC country has the lowest PE risk threshold?

Indonesia, under domestic law. Indonesia treats services provided in Indonesia for more than 60 days within 12 months as a PE trigger, although bilateral treaties typically raise this to 183 days. India is also notably aggressive in practice, with a 90-day service PE threshold under the US-India treaty (reduced to 30 days for related-party services) and a track record of expansive interpretation.

Q8. Is permanent establishment risk the same as tax residency?

No. Tax residency typically determines whether an entity is taxed on its worldwide income in a country (for corporations, usually based on incorporation or place of management). PE determines whether a non-resident company is taxed in a country on profits attributable to its activities there. A company can be tax resident in one country and have PEs in several others. They are related but distinct concepts.