Key Takeaways:

- Global payroll rarely fails at the calculation step. It fails at the seams between systems, vendors, and countries.

|

- The seven most common global payroll failure modes in 2026: FX lag, statutory filing miss, bonus misclassification, HRIS-to-payroll data drift, country-specific deduction errors, vendor fragmentation, and compliance regression after a regulatory change.

|

- Each failure has a predictable root cause and a specific prevention play.

|

- The latest 2026 regulatory backdrop, including the recently implemented OECD November 2025 Model Tax Convention update, the upcoming EU Pay Transparency Directive enforcement, and ongoing US and APAC state-level changes, is widening the compliance failure surface for companies running cross-border payroll.

|

- Consolidating payroll under a single operator with in-country expertise and a dedicated account manager resolves more of these structural failure modes than any other single change

|

Last updated: June, 2026

Introduction

Global payroll rarely breaks down during calculations; instead, it fractures at the seams connecting disparate systems, local compliance regulations, and cross-border teams. Here is the operator’s playbook outlining why global payroll goes wrong and the exact steps to prevent these infrastructure failures.

The seven failure modes this guide will cover are the global payroll problems that repeat across companies, markets, and vendor relationships, because the root causes are structural, and we need a systematic way of preventing them.

1. The Real Reason Global Payroll Goes Wrong

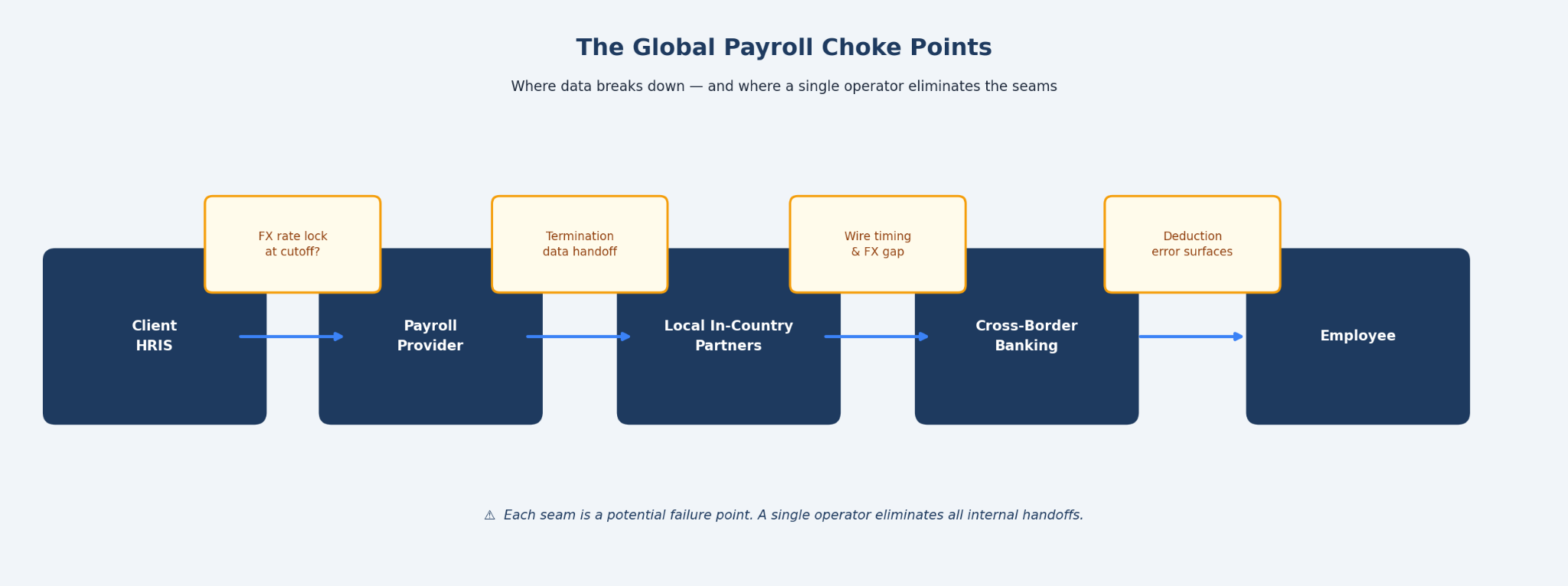

Think of global payroll as a relay race. The baton moves between your HR team, your HR solution platform, your payroll provider, local in-country partners, banks, and government agencies. Every handoff is a potential point of failure.

Calculation complexity (exchange rates, tax brackets, deduction schedules that vary by market) is where most attention goes. Those problems can largely be solved by payroll software today. The harder problem is the coordination layer: whether a termination entered in your HR platform on Thursday afternoon reaches a local payroll partner in Vietnam before their Friday cutoff; whether a regulatory update from the Taiwan Ministry of Finance that took effect in January is actually reflected in your payroll system, or whether it's still running on last year's rules.

Global payroll compliance issues happen in the gaps. The seven failure modes below each represent a specific gap.

Show Image Figure 1. The choke points where global payroll data typically breaks down, and where consolidating under a single operator eliminates the handoffs.

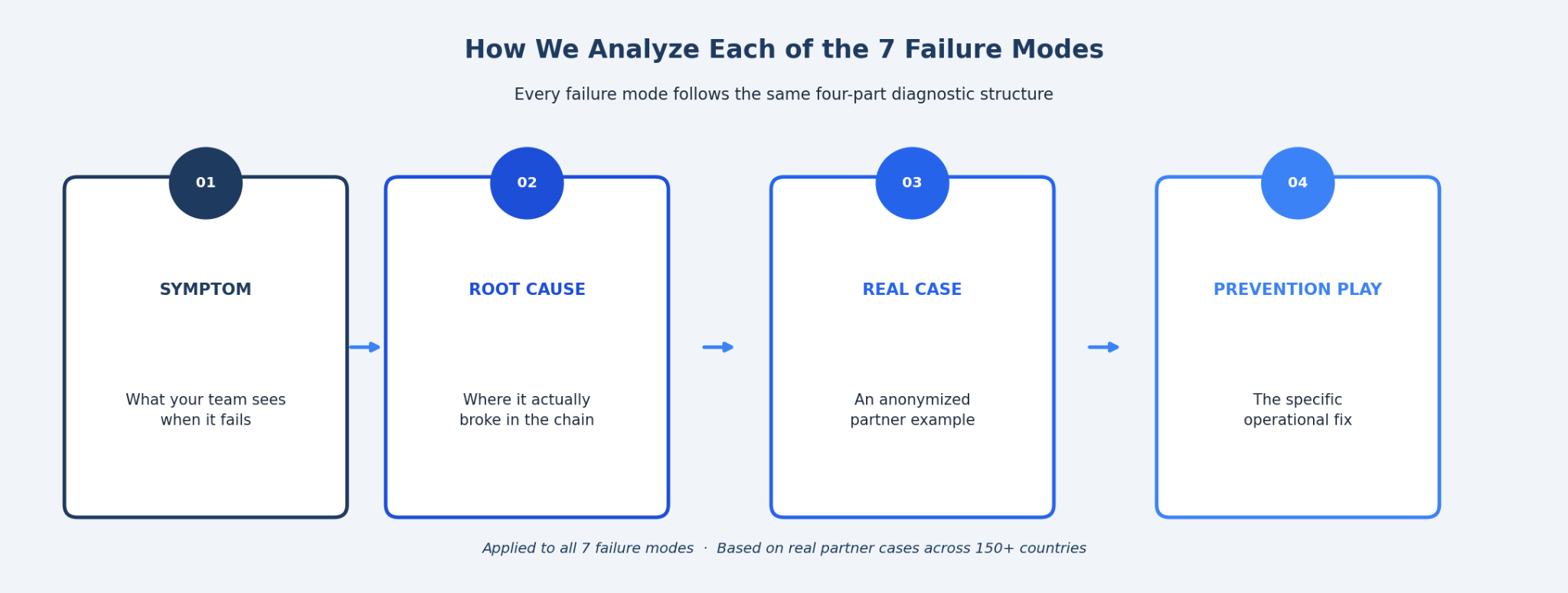

2. How This Guide Analyzes Each Failure Mode

The seven failure modes that follow are each analyzed through the same four-part diagnostic structure:

Figure 2. The four-part diagnostic structure is applied to every failure mode in this guide.

- Symptom: what your payroll or finance team sees when it breaks.

- Root cause: where in the chain the handoff actually failed.

- Real case: an example drawn from the kinds of situations we see across our partner network.

- Prevention play: the specific operational step that stops it from repeating.

3. Failure Mode 1: Currency Lag and FX Surprise

Symptom: Finance approves a payroll run. Five days later, the wires are clear, and the actual cost is 3-5% above the approved figure. Another common scenario is an employee contacts HR because the amount they received doesn't match what was agreed.

Root cause: Payroll is calculated against a rate at cutoff, but payment clears days later. In markets with volatile currencies (For example, Vietnamese dong, Indonesian rupiah, Indian rupee), a three-day gap is enough to produce variance that compounds across cycles. Companies managing payroll in USD and converting at wire time run an unhedged currency position on every payroll cycle.

Real case: A 250-person SaaS company approved a USD-denominated payroll run for its Malaysia and Singapore teams in mid-February 2026. By the clearing date, the Malaysian ringgit had moved 2.7%. The single-market cost coverage for that month was more extensive than the team's annual payroll software subscription.

4. Failure Mode 2: Statutory Filing Miss (Country Calendar Mismatch)

Symptom: A penalty notice arrives from a local labor authority weeks after payroll has closed. Or an employee flags that their social insurance contribution didn't appear in their account.

Root cause: Most payroll teams run one calendar for all markets, anchored to a Western month-end. However, each country has its own rules. For example, Japan’s resident tax withholding is due by the 10th of the following month. Singapore's CPF contributions are due by the 14th. Vietnam's social insurance follows the Labor Code cycle, not a Western convention. In short, a calendar built for London doesn't cover your operations in Tokyo.

Real case: Running on a UK-aligned cycle for 18 months, a 180-person company discovered it had missed Japan's resident tax filing window for two consecutive quarters. The resulting retroactive remittance, combined with accrued interest and late penalties under Japan's withholding tax rules, added up to a substantially larger liability than timely compliance would have been.

💡 Prevention Play: Global Compliance Calendars

-

Build a country-specific compliance calendar before your first hire in each market.

-

Automate filing reminders at the country level, not as a variation of your internal month-end.

-

Confirm with your provider that their system tracks local filing deadlines separately, instead of a generic single global schedule.

-

Read about how to navigate cross-country public holiday calendars.

5. Failure Mode 3: Bonus and 13th-Month Pay Misclassification

Symptom: A year-end audit finds that mandatory bonus payments were underpaid, omitted, or treated as discretionary, which changes both the tax treatment and the employee's legal entitlement.

Root cause: Statutory bonus obligations are market-specific and non-intuitive if you’re entering a new market. Take different countries as examples. In the Philippines, the 13th-month pay is a legal entitlement under Presidential Decree 851 as enforced by the Department of Labor and Employment: one-twelfth of annual basic salary, due December 24, for any employee with at least one month of service.

Indonesia's Tunjangan Hari Raya (THR), governed by Minister of Manpower Regulation No. 6/2016, is a mandatory holiday allowance equivalent to one month's salary, due at least seven days before Eid al-Fitr, not at calendar year-end.

None of these is discretionary. Common payroll mistakes in this category typically aren't caught until the first year-end cycle.

Real case: A technology company with a Philippine customer success team processed the 13th-month pay as a conditional year-end performance bonus, paid in January. An in-country legal review in Q4 caught the misclassification: the payment was a statutory obligation that couldn't be made conditional or delayed past December 24.

💡 Prevention Play: Bonus Obligations

-

Document mandatory vs. discretionary bonus obligations per market before the first hire. Include the calculation formula and legal deadline for each.

-

Have your HR and finance team know the guidelines and review annually, because statutory entitlement rules can change on a yearly basis.

-

Read more about our 2026 public holiday guide for the top 5 Asian markets.

6. Failure Mode 4: HRIS-to-Payroll Data Drift

Symptom: A terminated employee receives a paycheck two cycles after their last day. A salary change approved in March doesn't appear in payroll until May. A ghost record from a system migration keeps generating payroll entries.

Root cause: Most HRIS and payroll platforms run separately, with a manual sync. A termination entered on Thursday afternoon may not reach the local partner until Monday. A compensation change captured in the HRIS on a different day than the payroll file extraction creates a cycle-to-cycle gap. In multi-market setups, a single data point that needs to reach three different in-country partners has three independent failure points.

Real case: An employee in Vietnam resigned on the 8th of the month. The company communicated the termination on the 12th, four days after the local partner's data cutoff of the 10th. The employee received a full month's final salary. Recovering the overpayment under the Vietnam Labor Code required a formal recovery agreement, which adds unnecessary admin burden to both internal and external partners.

Note: For termination procedures across APAC, see our breakdown guide of termination laws by country and the employee off-boarding checklist ultimate guide.

💡 Prevention Play: HRIS-to-Payroll Data Flow

Treat HRIS-to-payroll data flow as an integration problem instead of an operational one. API-level integration is usually the structural fix.

If you currently don't have the means for API integration, alternatively, you can enforce a line-by-line pre-payroll audit against the payroll file at every cutoff, with close attention to terminations, new starts, and compensation changes in the prior 14 days.

Caught a payroll discrepancy and unsure what else might be lurking in your global setup? Book a quick discovery call with our global payroll expert to map your potential blind spots, market by market.

7. Failure Mode 5: Country-Specific Deduction Errors

Symptom: Net pay doesn't match employee expectations. A statutory authority issues a notice of underpayment. Or an annual audit uncovers contributions calculated at the wrong rate for months.

Root cause: Generic payroll platforms apply a default deduction model that administrators configure per country. When that configuration relies on a baseline rule rather than current local law, errors can quickly compound. Take these countries as examples:

- Singapore's Central Provident Fund (CPF) uses age-banded rates: the contribution threshold changes at 55, 60, and 65.

- Japan's resident tax is estimated for a new employee's first year, then corrected the following June by the municipality.

- South Korea's National Pension Service (NPS) underwent a landmark reform: effective January 1, 2026, the combined contribution rate rose from 9% to 9.5% under the amended National Pension Act (passed April 2, 2025), with further 0.5% annual increases planned through 2033. Payroll systems that were not updated by January 1 were immediately under-remitting.

You can read more about our Employment Guides across 150+ countries on country-specific hiring, taxes, benefits, compliance, and all HR strategies.

Real case: A company running payroll for a Singapore headcount that included employees aged 55-60 applied the standard under-55 CPF rates across the board. Over eight months, this produced both employer over-contribution and employee over-withholding. Correcting it required a formal amended filing with the CPF Board, plus individual net pay adjustments across the full period.

💡 Prevention Play: Age-Banded Deductions

Maintain age-banded deduction tables for every market you operate in. Set a fiscal year-start reminder to verify contribution rates (or consult with your local compliance partner to get updates).

Before each payroll run in markets with tiered schedules, cross-check the roster for age milestones or compensation changes that affect the applicable rate tier. Global payroll best practices in this area require market-specific configuration, so avoid using a shared global model.

8. Failure Mode 6: Vendor and Partner Fragmentation

Symptom: Month-end reconciliation takes the payroll team generally around three to five days because each country reports in a different format. One vendor's SLA miss delays salary in the market. Ledger discrepancies across partners can't be traced because each runs a different data model.

Root cause: Payroll vendors get added market by market during expansion. By the fifth or sixth country, the company has four or five separate relationships, each with its own SLA, reporting format, data cutoff, and escalation contact. Coordination cost compounds as headcount grows. This is one of the most common and major international payroll challenges that scales the worst.

Real case: A CFO at a 300-person company with employees across six APAC markets asked for a consolidated payroll report. What arrived were five spreadsheets, each in a different format, with different line-item labels for statutory deductions. The team had built a manual model to reconcile them. When a Malaysia rate changed, it went into the model but not into one vendor's configuration. The discrepancy ran undetected for two cycles.

💡 Prevention Play: Platform Consolidation

Consolidate under a single platform provider before fragmentation becomes structural. If you're already managing multiple vendors and partners, run a consolidation audit: SLAs, reporting formats, data cutoffs, and escalation paths. Phase the switch by market.

The goal is to have one partner with real legal and compliance coverage in each country, not a single platform that subcontracts locally and passes coordination costs back to you.

Read about how to choose the best Employer of Record platform for emerging markets.

9. Failure Mode 7: Compliance Regression After a Regulatory Change

Symptom: An audit finds contributions remitted at rates superseded by a regulatory update months ago. Employees under-taxed during the year face a personal year-end liability. A government inquiry asks why the payroll system is running on an old rate schedule.

Root cause: Regulatory change happens on the regulator's calendar, not the vendor's patch cycle. For example, Taiwan's Ministry of Finance issues circulars that can take effect within weeks. South Korea's minimum wage resets every January 1. Vietnam's Social Insurance Law 2024 (Law No. 41/2024/QH15), which took effect July 1, 2025, tightened contribution base rules and expanded participant coverage

Real case: A company's Vietnam payroll continued on a Social Insurance rate that was revised in early 2026. The platform hadn't updated its Vietnam configuration, and the change (which usually happens in July each year) wasn't caught in the pre-run audit. The under-remittance surfaced during a mid-year compliance review, requiring an amended filing and several months of back contributions to Vietnam Social Security.

💡 Prevention Play: Regulatory Monitoring

Regulatory monitoring should be a service your provider delivers, not a task your team maintains manually. At the fiscal year start, confirm with your provider that all contribution rates, withholding schedules, and filing deadlines are current. Add a mid-year checkpoint for markets with frequent mid-cycle changes.

Our payroll tax compliance guide covers jurisdiction-level requirements across major markets. If you're thinking about expanding into a specific market, remember to read our Employment Guide and learn more about the latest regulation updates, hiring tips, and compliance traps.

10. The 2026 Regulatory Backdrop Widening the Failure Surface

Three regulatory developments are creating the most immediate global payroll compliance issues in 2026:

- OECD November 2025 Model Tax Convention update: The revised Article 5 commentary introduces a two-part test for home office permanent establishment (PE) exposure. For companies with remote employees abroad, this is the most consequential treaty change in a decade. Country-level interpretation is still being implemented.

- EU Pay Transparency Directive (2023/970): EU member states are transposing this Directive into national law from 2026. Key obligations include gender pay gap reporting for employers with 100 or more employees, employee rights to request pay comparison data, and restrictions on pay history inquiries.

- US state-level changes: California's ongoing AB-series worker classification rules, New York's pay transparency and disclosure requirements, and Illinois's Equal Pay Act amendment (HB 3129, effective January 1, 2025), which requires employers with 15 or more employees to include pay scale and benefits in all job postings, are each creating additional compliance layers for companies with US-based employees.

|

Jurisdiction

|

Update

|

Effective

|

Payroll Impact

|

Source

|

|

OECD (global)

|

2025 Model Tax Convention update: revised Article 5 PE commentary

|

November 2025

|

PE risk for remote employees abroad

|

OECD

|

|

EU (member states)

|

Pay Transparency Directive (2023/970) national transposition

|

Ongoing from 2026

|

Pay reporting and disclosure obligations

|

EUR-Lex

|

|

Singapore

|

CPF contribution rates for senior workers (55-65) increased by 1.5 percentage points; the Ordinary Wage ceiling was raised from SGD 7,400 to SGD 8,000

|

January 1, 2026

|

Employer CPF costs for employees aged 55-65 increase; age-banded payroll misconfiguration will under-contribute

|

CPF Board

|

|

Japan

|

Annual minimum wage revision (reviewed each fiscal year, effective October); income tax withholding due by the 10th of the following month per NTA

|

October annually

|

Payroll teams have a narrow window to update minimum wage configurations before the October effective date

|

MHLW

|

|

United States (California)

|

AB5 and subsequent classification rules

|

Ongoing

|

Worker classification for gig and contractor roles

|

California Labor Code §2775

|

|

United States (New York)

|

Pay Transparency Law

|

In effect

|

Salary range disclosure for job postings

|

NY Department of Labor

|

|

United States (Illinois)

|

Equal Pay Act amendment (HB 3129): pay scale and benefits disclosure required in job postings for employers with 15+ employees

|

January 1, 2025

|

Affects distributed teams with Illinois-based roles or supervisors, including remote workers reporting to an Illinois office

|

Illinois Department of Labor

|

The pattern is consistent: regulatory complexity is growing in multiple directions at once. APAC contribution rates update mid-cycle, often with limited advance notice. EU directives are transposed at different speeds across member states. US requirements fragment further by state each year. For companies running payroll across three or more markets, staying current without a partner who actively tracks each jurisdiction doesn't just create compliance risk. It widens the blast radius of every failure mode described in this article.

11. The Operator's Prevention Playbook

Seven failure modes, seven prevention plays. The table below maps each one so your team can use it as an audit checklist against your current setup.

|

Failure Mode

|

What You See

|

Root Cause

|

Prevent Play

|

|

Currency lag and FX surprise

|

Cost variance between the approved and actual payroll

|

FX rate not locked at cutoff; converting at wire date

|

Lock FX at cutoff; fund local accounts in local currency

|

|

Statutory filing miss

|

Penalties, retroactive adjustments

|

The Western calendar doesn't track local deadlines

|

Country-specific compliance calendar for every market

|

|

Bonus and 13th-month misclassification

|

Year-end true-ups, statutory exposure

|

Mandatory bonus treated as discretionary

|

Document mandatory vs. discretionary entitlements per market before the first hire

|

|

HRIS-to-payroll data drift

|

Ghost employees, overpayments, missed changes

|

Manual sync between HRIS and payroll

|

API integration or enforced pre-payroll reconciliation at every cutoff

|

|

Country-specific deduction errors

|

Wrong net pay, audit findings

|

One-size-fits-all deduction model

|

Age-banded, tenure-sensitive deduction tables, reviewed at the fiscal year start

|

|

Vendor and partner fragmentation

|

Reconciliation delays, SLA misses, and ledger discrepancies

|

Multiple vendors with no unified reporting

|

Consolidate under a single operator with in-country expertise

|

|

Compliance regression

|

Outdated rates; payroll on superseded rules

|

Regulatory monitoring is reactive

|

Confirm rates at fiscal year start; mid-year checkpoint in volatile markets

|

12. How We Prevent These Failures

We run Global Payroll across 150+ countries through 600+ local legal and payroll partners, in 130+ currencies. Our processes are organized around the failure modes above, with a focus on catching issues before they reach payroll. Here is what that looks like in practice.

- One named Account Manager per client, from day one: Self-serve payroll platforms put compliance monitoring on your team. We put a person on it. Your Account Manager tracks every market you operate in, knows your payroll cycle, and surfaces regulatory changes before they affect your next run. In practice, this matters most for the failure modes that require someone to know what you don't.

- A defined monthly payroll cycle with named handoffs: Client data by the 10th, payroll report by the 15th, client approval by the 18th, invoicing by the 20th, paychecks finalized by the 25th. Every stage has a named contact and a clear escalation path when something needs to move faster.

- 600+ in-country partners monitoring regulatory changes across 150+ countries: When a MOM circular updates Singapore CPF rates or Vietnam's Social Insurance schedule shifts mid-year, our in-country partners surface it. Your payroll configuration is updated before your next cycle runs, not after a penalty notice arrives.

- One platform covering employees and contractors: Whether you're running salaried employees in Singapore, contractors in Taiwan, or a mixed workforce across different APAC markets, our Global Contractor Management and Global Payroll run on the same platform under the same Account Manager, integrating tools, insights, and support in one place. We are ISO 27001-certified, the data security benchmark your finance and legal teams typically require before approving a payroll provider.

"A Singapore tech company came to us after their previous provider had applied the standard under-55 CPF rates to a team that included several employees aged 55 to 60. By the time the CPF Board surfaced the discrepancy, the miscalculation had run for eight months. We audited the headcount by age bracket, filed the amended contributions, and rebuilt their payroll configuration around Singapore's tiered CPF schedule."

— Slasify Account Manager

Frequently Asked Questions

1. What is the most common cause of global payroll errors?

The most common root cause isn't a calculation mistake. It's a coordination failure at a handoff point. HRIS data doesn't reach the local partner on time. An FX rate shifts between approval and payment. A contribution rate changed in January, but the platform hasn't updated. Most global payroll mistakes are predictable in category, even when the specific instance is a surprise.

2. How can a company prevent FX-related payroll surprises?

Lock the FX rate at payroll cutoff and pay in local currency from a locally funded account. If your provider converts at wire time, you carry currency risk on every cycle. For volatile markets, build a tolerance threshold: any FX movement beyond a defined percentage between approval and payment triggers a secondary authorization.

3. What's the difference between a global payroll provider and an Employer of Record?

A payroll provider handles calculations and disbursements. An Employer of Record is also the legal employer in the target country, taking on labor law compliance, statutory benefits, and local obligations. Most cross-border hires need both. Running them through separate providers introduces the same handoff friction this article describes. We provide Global Payroll and Employer of Record on a single platform, under one Account Manager.

4. How do you handle statutory bonus payments across multiple countries?

Country-specific statutory bonus obligations are built into the monthly payroll cycle, not managed as a separate annual task. Mandatory payments like the Philippines' 13th month pay, Indonesia's THR, and Brazil's 13th salary are calculated on the legally required basis and remitted by the statutory deadline. Clients submit bonus updates by the 10th; the cycle then processes, approves, and finalizes payment by the 25th.

5. What new payroll regulations should companies prepare for in 2026?

Three developments are creating the most immediate compliance exposure in 2026: the OECD November 2025 PE update, EU Pay Transparency Directive transpositions, and US state-level changes in California, New York, and Illinois. If your employees work in or report to these jurisdictions, your payroll setup may already be affected. You can check the regulatory table in Section 10 above for a quick overview and reference (with sources).

6. Can one platform handle global payroll for every country?

There’s no single platform that can solve everything, as it depends on the countries in which you operate. However, we deliver localized payroll across 150+ countries using 600+ vetted in-country partners to ensure compliance with volatile local tax regulations. Book a free demo to confirm availability for your target markets and your potential next steps for your expansion plans.

7. How does Slasify prevent the failures listed in this article?

Our in-country expert network, defined payroll calendar, and dedicated Account Manager per client cover the majority of the failure modes in this article. The genuinely hard cases are extreme FX volatility in select frontier markets and mid-cycle regulatory shifts without advance notice. No provider has fully solved either. Our 600+ local partners are the closest approximation to real-time ground-level monitoring that currently exists.

Stop Treating Global Payroll as an Afterthought. Secure Your Infrastructure.

You know where the gaps are. The next step is mapping them against your current setup, market by market. Failures aren’t just administrative headaches. In many cases, they are predictable revenue drains. Treat your global payroll deployment with the same rigor that software engineers treat production code. Ready to eliminate cross-border data drift and FX lag? Book a tailored compliance audit with our specialist today.